Pole Position in

Medical Technology

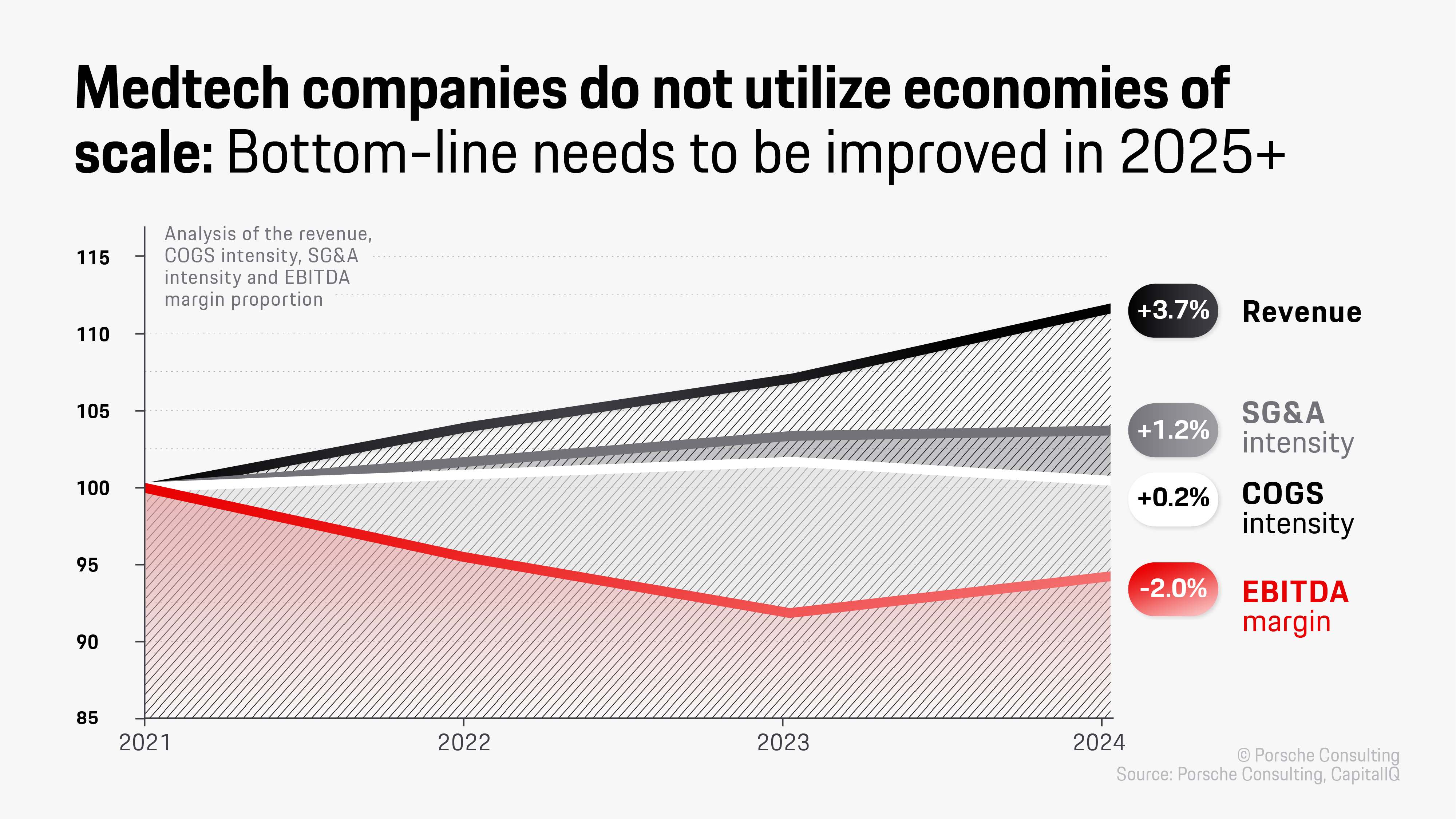

What is the state of the medtech sector? In an analysis of the 100 largest medtech companies worldwide, Porsche Consulting examined the current state of the industry. The key financial figures show: Revenues have grown by an average of 3.7 percent since 2021. Hardly any economies of scale have been realized on the cost side. Margins are falling. CEOs who seek to outperform the market need to act now.

01/2025

Of the top 100 players in medtech, US-American companies dominate the market. Large European competitors often struggle to match the pace of financial performance. Only a few European medtech companies have succeeded in posting disproportionate earnings before interest and taxes (EBIT). These are some of the results of a recent study by medtech experts at the Porsche Consulting top management consultancy.

There is no doubt that the sector has enjoyed strong growth over recent years. Demographic changes in many major markets and greater prosperity in several high-demand regions of the world have fueled this development. The COVID pandemic was another driving force behind medtech — in marked contrast to the majority of other industries. But now all signs are pointing to more challenging times. This is already clear from the numbers: despite rising sales, earnings at the world’s largest medtech companies are stagnating. Costs are the main factor here. They are rising in proportion to revenues and effectively preventing economies of scale. In other words: economies of scale have essentially not been achievable on the cost side.

The analyses show that the medtech sector expects challenges in 2025 and beyond. Rising healthcare costs around the globe are triggering greater cost sensitivities and price pressure, especially for public and tax-funded healthcare systems. Geopolitical developments are also in play. And regulatory requirements are on the rise, for example in government directives and authorizations in the USA and Asia.

But challenges bring opportunities. In 2025 companies will also be able to gain significant competitive advantages, outperform the market, and increase market capitalization. Four fields of action are crucial here, and should be part of each medtech CEO’s agenda in 2025.

1. Innovation: Speed is the new competitive edge

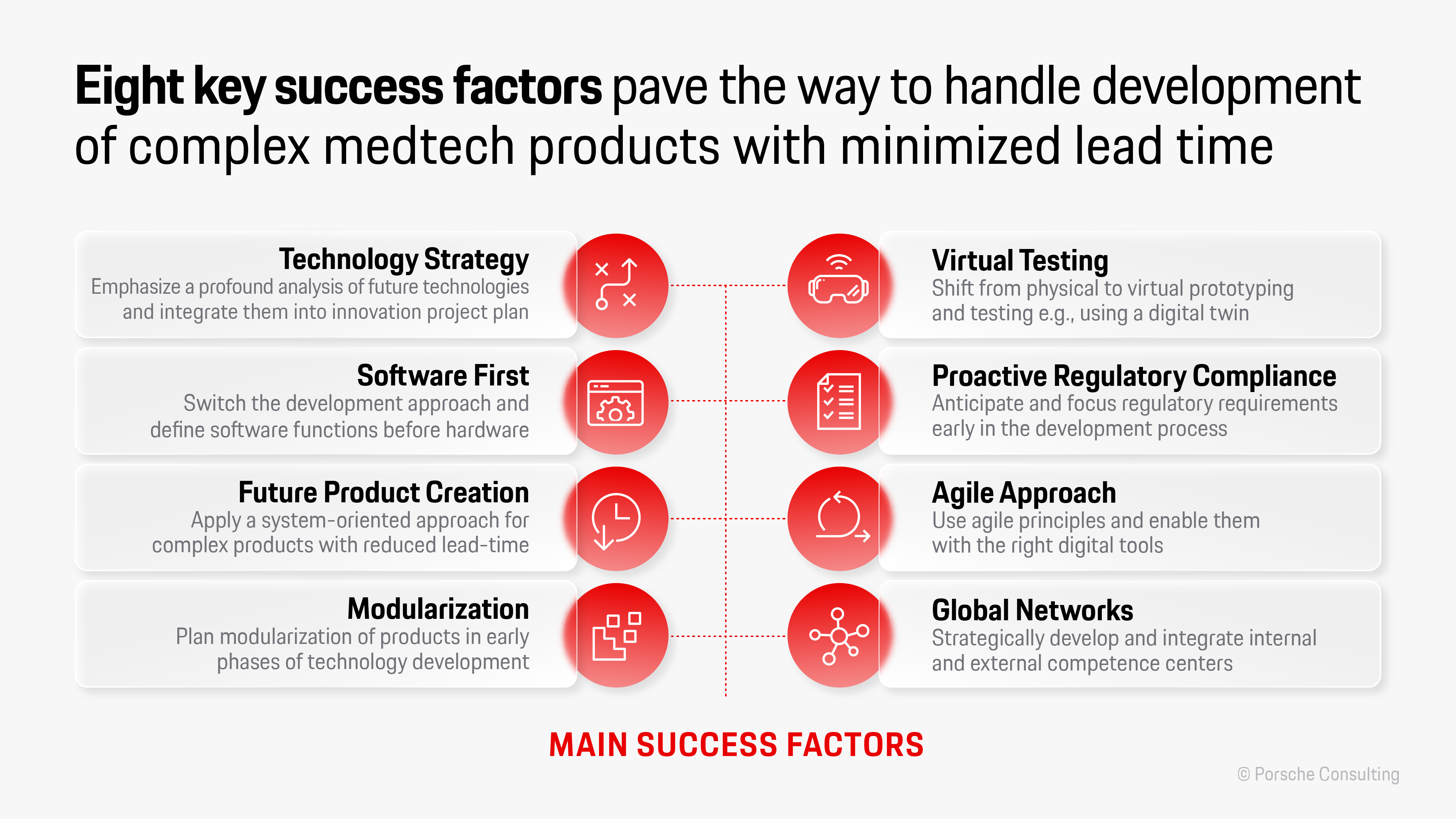

A key factor for future success is the acceleration of product development. Benchmarks for the introduction of innovations are currently being set by new innovators from IT and health tech. To counter this rise in competitive pressure, medtech companies need to develop their own good ideas rapidly to market readiness. Right now these processes take as much as a decade, including development of the requisite technology. That is too long. Moreover, the relevant processes often show huge inefficiencies.

To optimize “time to market” on a sustainable basis, companies need to take the entire product engineering process into account. The first step is a targeted product strategy in order to begin developing technologies at favorable times and ensure their integration into products. A system-oriented approach can solve integration problems early on in the concept phase and thus save the time spent on identifying deficiencies in later product development stages. One key accelerator will consist of virtualizing the creation and testing of prototypes. As the virtual imaging of medical devices and the digital twins of patients become ever more precise, increasingly powerful tests can be conducted well before the clinical trial stages.

In addition, the entire product engineering process needs to become more efficient. Development methods used in the software sector set the right standards here. Medtech companies will need to prioritize software in the future — and conceptualize the entire patient-care system around it, for example in hospitals. This will improve interoperability and thereby also increase hospital efficiency. System-based definitions of the relevant requirements, including those of regulatory stakeholders, plus the use of platform and modularization strategies will secure cost advantages and make the benefits available sooner to patients.

The new focus on software, however, is also leading to higher levels of product complexity. This in turn requires the right skills and priorities in software development. Medical technology in the future will ideally be smart and connected — and therefore compatible with the healthcare information systems of tomorrow.

2. Production and supply chains: Lowering costs, raising profit margins

Unused economies of scale in production and supply chains are one reason for the stagnant profit margins in the medtech industry. When expanding their production capacities, many companies failed to design processes to be more efficient. The high demand and favorable prices did not encourage a focus on efficiency. That now needs to change.

Major levers for optimizing production costs include balancing personnel costs, taking a make-or-buy approach in keeping with company strategy, negotiating prices systematically with suppliers, and shaping production networks so as to uncover additional productivity via synergies and ideally foster attributes such as customer satisfaction thanks to shorter delivery times.

CEOs also need robust and flexible production networks in order to address geopolitical exigencies and regulatory demands. Many medtech companies have a long way to go in this regard. In recent years, medtech companies have often accelerated their growth through M&A activities. But in the post-merger processes, they have neglected to utilize operational synergies. This often results in production networks that for historical reasons feature individual, differently structured, and independently run sites.

Many companies have not yet focused their production networks on the future. Local-for-global strategies that used to yield advantageous personnel costs now have to be reassessed in light of many states’ new protectionist ambitions and the rising complexity of local regulations. Each company needs to apply a clear focus to optimizing its global footprints, based on its specific strategic aims. This can incorporate a number of different perspectives:

Deliverability of items such as crucial raw materials can be safeguarded by avoiding trade barriers or ensuring production capacities. This often entails registering or internally planning for additional sites or additional (excess) capacities from partners, in order to secure the strongest sales markets.

Companies need to ensure that all production sites meet local regulatory requirements for quality, production, and packaging processes throughout the entire value chain of any given product. It is important for companies to maintain or develop local expertise in order to meet these operational requirements. Initial steps usually involve building smaller sites with bridge functions and establishing relations with local authorities.

Sustainability is another important issue. Internal and external environmental, social, and governance (ESG) goals can be met by gaining access to renewable sources of energy, optimizing transport routes and means, and working with certified partners. Optimization with an ESG focus can also mean addressing potential ethical questions.

Procurement and production costs depend on factors such as local labor markets, energy infrastructures, import costs, and raw material availability, as well as the strength of the currencies involved. Optimizing costs does not necessarily mean cutting them. When deciding on sites, incentives and subsidies from local authorities or states can also play an important role.

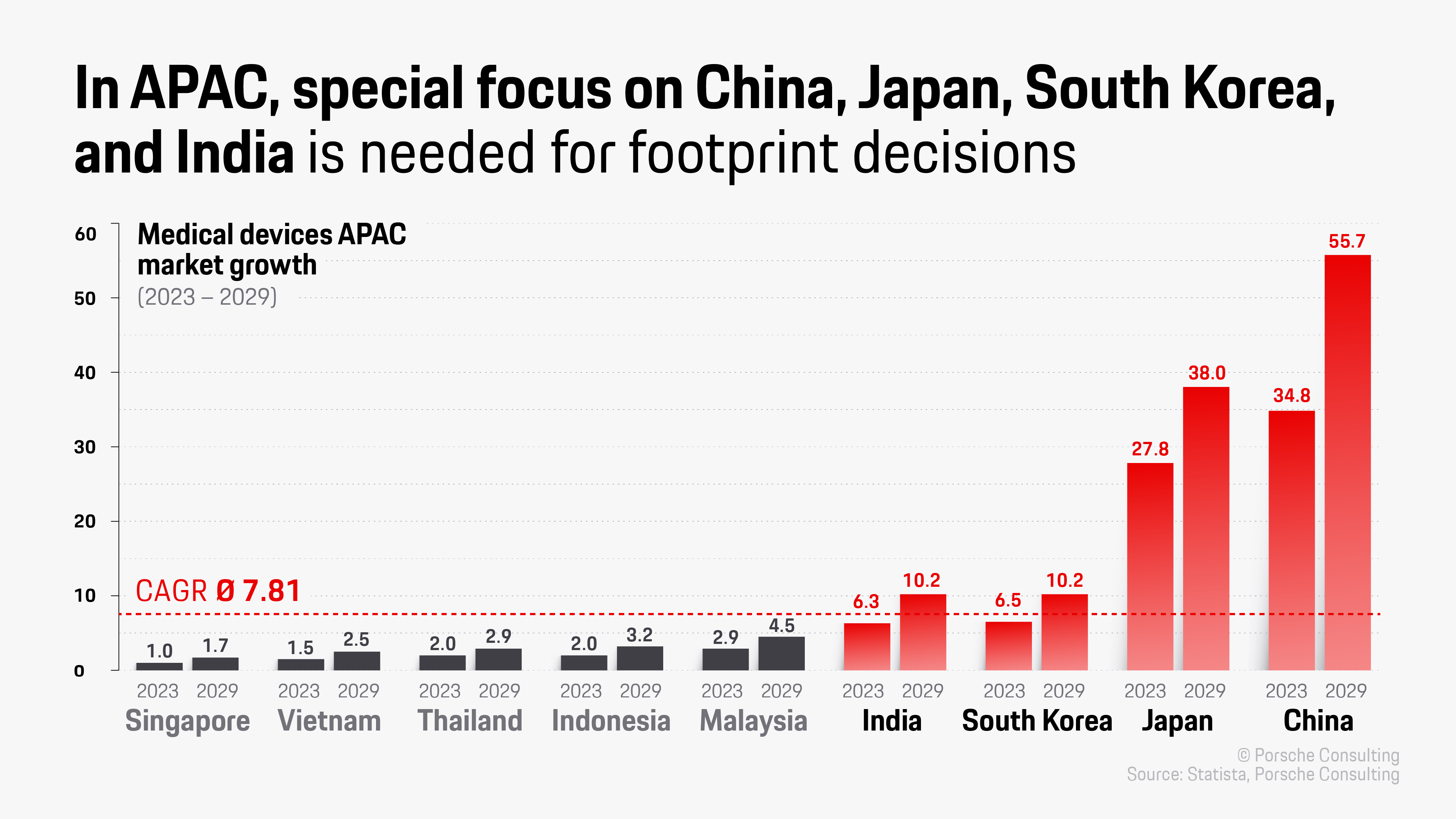

There are many more questions to consider within the context of a footprint strategy. Major factors here include the appetite for risk and the ability to assess probabilities in corresponding scenarios. One specific question for 2025 is, in addition to a dedicated US strategy, how to design the manufacturing footprint in the Asia-Pacific region (APAC). A very discerning approach is needed here: the APAC market as a whole will not outperform either the US or the European market in the foreseeable future. However, individual and regional production strategies should be applied to the four strongly expanding markets of China, Japan, South Korea, and India — not least of all from the perspective of accessibility to these markets.

Despite greater sensitivity to cost, further improvements are needed in the quality of both products and processes. Not only for the benefit of patients, of course, but also in medtech companies’ own interests. Regulatory authorities are increasing the frequency and intensity of their inspections. In extreme cases, entire markets can be closed if authorities raise relevant objections. In the USA alone over recent years, the FDA has increased annual inspections of foreign firms by 243 percent. Eighty-nine percent of these inspections were based on violations of quality systems.

In order to ensure quality, it is especially important for medtech companies to establish mechanisms and standards as well as to motivate and empower employees to apply them throughout the entire production process.

Best-in-class medtech companies often do both at once. First, they define globally harmonized standard operating procedures (SOPs) with sufficient scope to meet local regulatory demands. And second, they establish central quality management systems that furnish work stations with the digital tools employees need to embrace quality efficiently and effectively.

The priority must be placed on making quality an integral part of every step in the process. Quality departments should not function solely as monitoring and documenting units, but rather be viewed as value-adding business partners for the company as a whole.

3. Digital transformation: Prioritize execution and scaling

Medtech companies have yet to make sufficient use of the potential offered by digitalization. Despite comprehensive attempts at digital transformation, most medtech companies are not showing noteworthy measurable successes. On the cost side, AI-supported process innovations are an option. And on the revenue side, software solutions are among the promising examples. Two-thirds of the world’s largest 25 largest medtech companies report that digitalization accounts for only 0 to 10 percent of their overall revenue. Only at two companies does that figure exceed 20 percent.

What should medtech companies do to achieve short- and medium-term success through digitalization? Here are the top three recommendations for 2025:

Invest more systematically in AI

Systematic application of AI transformation programs can significantly reduce costs and increase productivity by up to 20 percent, and in some areas (such as marketing and sales) by 30 to 40 percent. The greatest potential for AI in the medtech sector lies in product development, analysis of patient data, and product commercialization. These actions require a clear strategy, 100 percent commitment on the part of top management, relevant investment volumes, strict AI portfolio management (priority on use cases with the greatest business impact), an AI organization anchored in all areas of business, and a high-performing and flexible technological infrastructure.

View “software as a medical device” as its own business field

The “software as a medical device” (SaMD) market will grow to more than 700 billion USD by 2030. The strongest growing SaMD subsegment is “AI-enabled medtech devices,” with annual growth of 48 percent and 950 FDA authorizations thus far. An alarming note here is that only 27 percent of these authorizations have come from conventional medtech companies. The greatest share has come from start-ups or big tech.

SaMD is a future-oriented field that will change the industry’s revenue structures and should therefore be the focus of much greater attention by medtech companies. Some basic foundations need to be laid, including investments, establishing a separate business unit, building software and AI development expertise, and professionalizing the commercialization side.

Build partnerships and ecosystems — do the basics right

The exponential rise in technological demands on medtech companies shows no signs of abating. Products are becoming ever more complex due to greater shares of software and AI. For diagnostic imaging equipment (e.g., MRT and CT systems), for example, lines of code have increased in number from a few dozen just ten to twelve years ago to more than 15 million today in order to handle processing, analytics, and cloud connectivity needs.

Now and over the next three to five years, most medtech companies will not be able to meet these rising demands just on their own without entering into partnerships, for example with start-ups and tech companies. Porsche Consulting has observed that the quality of collaborative efforts with tech companies can leave something to be desired. Ways to improve collaboration with start-ups include accepting cultural differences and speeds of work, setting clear and shared goals, developing strong collaborative mindsets, and creating better organizational frameworks for the exchange of ideas.

4. People: The key to achieving ambitious goals

The medtech sector’s personnel needs have increased by 30 percent over the past five years, and will continue to rise. However, the availability of skilled workers will decrease by 6.9 percent by 2030. The resulting bottleneck will have consequences. Chief among them will be tough competition for talented individuals with pronounced digital expertise and skills in data and AI. Cognitive abilities such as creative thinking and lifelong learning are also high on the list of the World Economic Forum’s core skills of the future.

Strong employer attractiveness is the key to recruiting and retaining talented personnel for all the areas needed. The top 10 medtech companies are considered attractive by graduates in engineering and the natural sciences in Germany, for example, but the field does not enjoy the same high appeal in the eyes of business and IT graduates. Skilled workers in the latter two disciplines are more likely to favor global companies in the tech and automotive sectors.

In addition to enhancing employer attractiveness, another challenge for medtech companies and their HR departments lies in addressing rising cost pressures. The response here needs to encompass a more systematic approach to digitalizing personnel processes and company decisions — such as the selection of new sites — with the help of HR analytics. With its advisory role in reorganizing and reducing personnel, HR departments can exert considerable leverage on their companies’ structures and costs. And therefore also on their overall competitiveness.

The mission for medtech CEOs is now to position their companies to attract talented employees:

- Purpose: Medtech employees make major contributions to improving human health and quality of life.

- Challenges: Medtech is an innovative sector that integrates new technologies into digital ecosystems. The data thereby compiled are enabling a revolution in healthcare, often with the help of AI. The industryoffers a diversified working environment with extensive opportunities for personal growth.

- Stability: The ever-growing demand for medical technology ensures job security and attractive salaries.

- Versatility: Complex medtech solutions require close collaboration among experts from different fields, and their international scope encourages intercultural exchange.

In a nutshell: the medtech industry fulfills all the criteria for an attractive employer. These features need to be made explicit — for job applicants as well as for employees already working at companies in the medtech sector.