Brake or Accelerate

Have fleet operators miscalculated their electric vehicle numbers? A drop in demand and a slump in used-car prices are putting pressure on the car-leasing, rental, and sharing sector. Added value, experts say, could enable the sector to recharge its business and encourage customers to join the energy transition.

05/2024

The situation is challenging, but Ömer Köksal remains confident. “We’re continuing to successively convert our fleets to electric vehicles,” he says. His company is the Allane Mobility Group, which specializes in car-leasing and full-service solutions. It launched and is pursuing a transformation to electromobility. As the managing director of Allane Mobility Consulting GmbH, Köksal is in charge of B2B for Germany’s largest brand-independent provider of new and used vehicles.

Full warehouses, few customers

Headquartered in the southern German metropolis of Munich, Allane Mobility Consulting has 33,700 contracts in the fleet leasing sector and 48,500 in fleet management. It advises major companies on how to manage their fleets efficiently, and provides all relevant services for the operation of passenger cars and vans. Its customers include corporations such as SAP — which alone has a good 18,000 vehicles — as well as Siemens and Lufthansa. “The situation isn’t easy at the moment,” says Köksal. “With e-car subsidies no longer available since the start of the year and in light of the inadequate charging infrastructure in Germany, there’s a lot of uncertainty. There’s been a considerable decline in the demand for electric vehicles. Dealers’ garages and warehouses are full, but they don’t have the customers right now to lease or buy the cars.” The vehicles are in “park,” not “drive.” Not a good option for an innovative product. Nearly all leasing companies, fleet operators, car rental companies, and car-sharing providers have been observing the situation Köksal describes for some time now. The energy transition alone can’t make the sector run on automatic. Despite their widely recognized benefits, electric vehicles have lost some of their appeal to drivers. For the first two months of 2024, sales in Germany were at their lowest level in three years.

Chain reaction hits late-model used cars

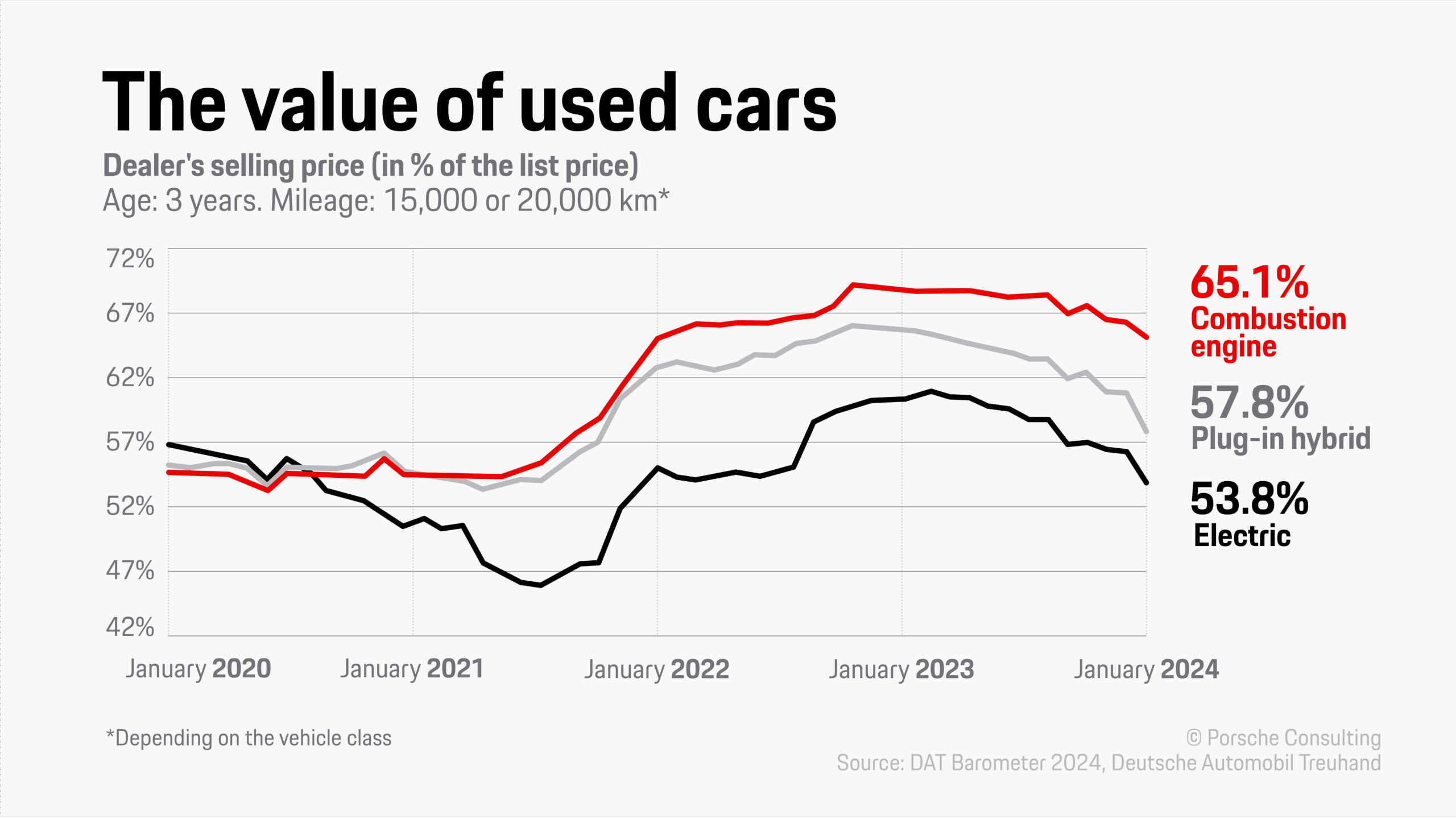

The decline in appeal has triggered a drop in demand for electric cars. One market-based consequence is that the prices for relatively new or late-model used cars have also dropped. Their levels are closely linked with the prices for new cars, points out Martin Weiss, a specialist in automotive data and the director of vehicle valuation for Deutsche Automobil Treuhand (DAT). As he explains, “We’re coming down from an abnormally high mark on the market, which had spiked because of the shortage caused by COVID, the chip crisis, and the resulting delivery problems. Now there’s an excess in supply, plus a considerable slump in the new car market. That puts new-car prices very close to those for used cars, which in turn makes it hard for used-car sellers to get what they originally anticipated.”

Also of note is the skepticism many customers have about matters such as battery capacity and lifespan. One concern is that today’s new cars could soon become “obsolete” due to rapid advances in technology. According to Germany’s Federal Motor Transport Authority (KBA), only 97,000 used EVs were sold in the country in 2023, which amounts to just 1.6 percent of the country’s used car market. As a consequence, late-model used e-cars are often only marketable at greatly reduced rates.

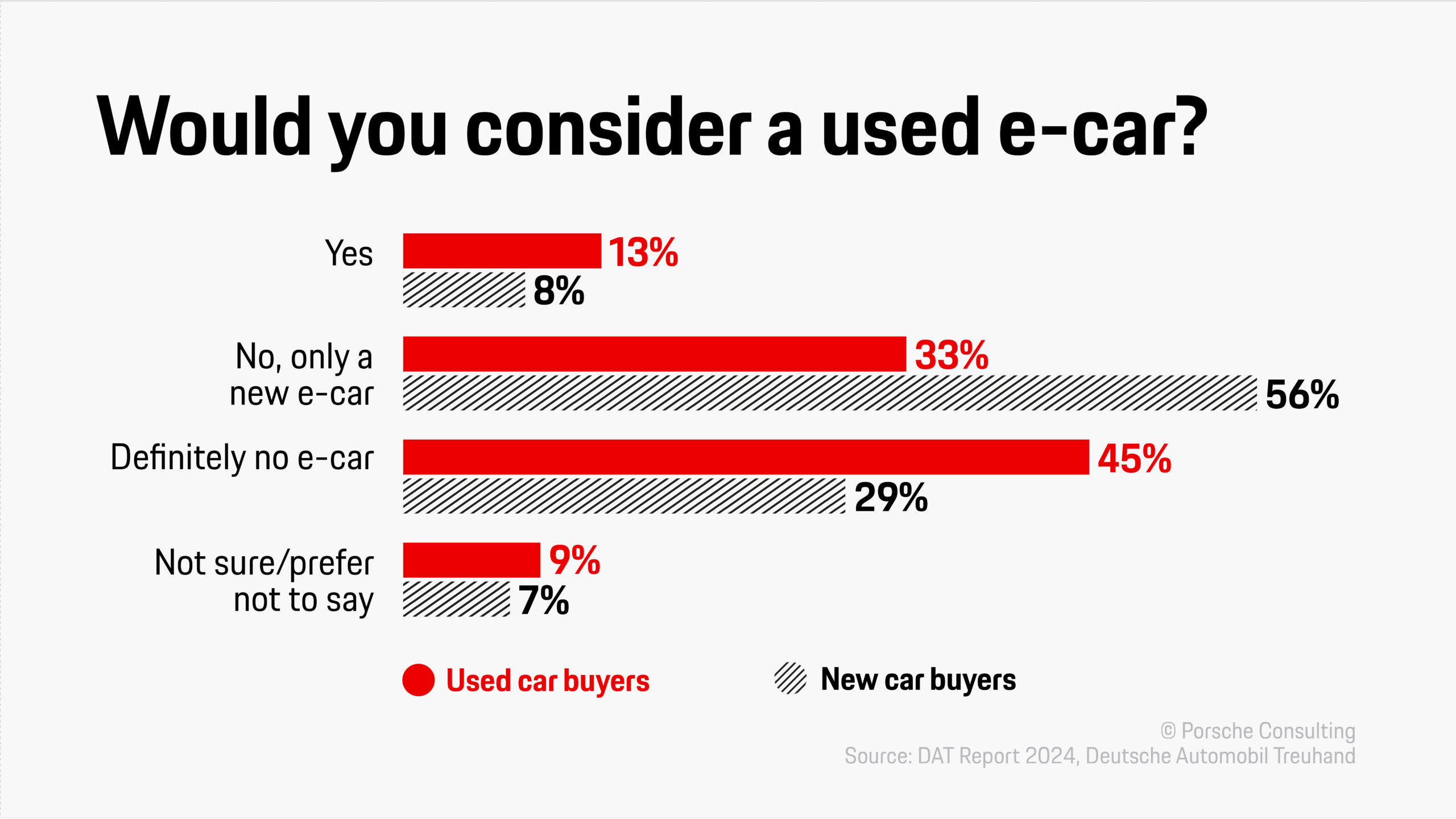

The car rental company Sixt, whose revenue derives in part from selling its used vehicles, has cited price reductions of “more than 20 percent.” According to a study by AutoScout24, an online marketplace for used cars, second-hand electric vehicles were nearly 30 percent cheaper in early 2024 than in the same period of 2023. Market observers expect this downward trend to continue in 2024 and 2025. According to a DAT analysis, only 13 percent of used car buyers are considering switching to an electric vehicle.

The numbers aren’t adding up

The situation is especially tight for mobility providers whose fleets have high numbers of electric vehicles available for renting or sharing. They are struggling to remain profitable. This is not only a matter of e-car residual values falling below anticipated levels and holding the numbers down. Bottom lines are also under pressure from what can be considerably higher vehicle operating costs. Factors here include lower capacity utilization due to longer downtimes from charging, complex car transfers to and from charging stations, and longer service times for high-voltage components that have to be repaired at authorized workshops. Companies also incur costs from investing in their own charging infrastructures and from the high prices at public rapid charging stations. Another non-optimal factor is the fact that vehicles are only rarely booked for extended periods. E-cars tend to be rented for a day, but seldom for four, seven, or fourteen days.

Leading car rental companies are taking steps to address the situation. After reporting a negative impact of around 40 million euros on its 2023 revenue due to lower residual values for electric cars, Sixt has increased depreciation and placed a significantly higher priority on “phasing out electric risk vehicles,” according to a press release by the international rental corporation. Sixt will doubtless continue to reduce its share of electric vehicles. Its US-based competitor Hertz also wants to cut its EV numbers — by 20,000, or roughly one-third of its total fleet. It will use the proceeds to purchase new cars with combustion engines. For Helena Wisbert from the Center of Automotive Research, these decisions by Sixt and Hertz represent “another setback on the road to electromobility.”

Fleets and ESG

Ömer Köksal is of the same opinion. He talks about a “dilemma” many companies are facing. On the one hand they need to respond to market conditions and are therefore pulling the brakes on electromobility. “At the same time, many companies are trying to increase electromobility in their fleets to meet the CO2 targets called for by governments and the public. According to the EU taxonomy, vehicles with climate-friendly drive systems can be considered environmentally sustainable investments. Fleets are therefore one of the instruments at companies’ disposal for implementing their ESG strategies.” Köksal is thus calling on policy makers to provide more support for transitions here, such as tax incentives or simpler reporting requirements. “We need clearer guiding principles,” he says.

The Allane Mobility Group wants to further expand the range of components in its mobility budgets in the future. It expects to provide not only cars to its corporate customers but also e-bikes, public transportation packages, and the popular “Deutschland-Tickets” or country-wide rail tickets. In developing these sustainable mobility solutions, the Munich-based company is working closely together with the Porsche Consulting management consultancy. As Köksal explains, “If we don’t want to jeopardize the rise of e-mobility, we need to create added value.” This view is shared by Helen Mayer, Senior Consultant in Mobility Services at Porsche Consulting. “We need to act now,” she says, “and we need new solutions that can make electromobility more attractive to customers. It’s also crucial for fleet operators to offer more mobility options to their customers’ employees.” She recommends the following: “Corporate transformations toward electromobility should not be allowed to sputter out. They should be accelerated. Leasing and financial service providers should optimize their internal processes and procedures. And new creative approaches are needed to address the uncertainty about how to handle electric vehicles.” Assets should be managed substantially more dynamically and applied systematically throughout vehicle life cycles. As she continues, “The time for empirical data alone is past. We need to look ahead. When it comes to electromobility, reverse gear is not an option.”

Lowering thresholds